Jason Noble explains the 4 non-negotiable pillars of retirement planning with host Tom Crawford of ABC Lowcountry Live.

- Watch the fees you are paying on your investments

It is very important to understand fees because you can have what’s called “fee drag” if you are paying too much. And it’s not just what the advisor is charging—you need to know what your “expense ratios” are—or what fees you are paying inside the investments themselves. These are hidden costs! And what about any administrative costs that are hidden inside the portfolio as well?

It’s fair to pay a financial advisor fairly for what they do. But is your financial advisor using cost-effective investments and strategies inside your portfolio to grow your wealth? Are they looking at ways to put more money in your pocket and less in theirs? That’s where a fiduciary advisor comes in.

Because fiduciaries are not allowed to make commissions on stock market trading, they charge a flat fee to manage market investments. This means if your portfolio value drops, their fee drops. They can only make more money if they make you more money—by growing your portfolio’s value.

A fiduciary standard is the higher of the two standards that the financial services industry is held to. The suitability standard that many financial professionals use simply means that at the time of recommendation, the investment was “suitable.” The fiduciary standard means that fiduciaries must recommend only what is “in a client’s best interest”—even if it’s not in the fiduciary’s best interest.

A financial advisor like Jason Noble is held to the fiduciary standard originally enacted in 1940; the “Investment Advisers Act of 1940.” And even more stringent than that are the requirements mandated by Jason Noble’s designations CFP® and RICP®, CERTIFIED FINANCIAL PLANNER™ and Retirement Income Certified Professional® respectively. These designations have fiduciary responsibilities baked into Jason’s ongoing continuing education, and the bylaws of their code of ethics.

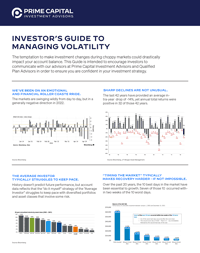

- Make sure portfolio matches your risk tolerance, and risk capacity

Obtaining your risk tolerance number is fairly straightforward. In fact, PCIA Charleston has a free tool you can use right here. Risk capacity is a little trickier. As you head toward or are in retirement, as a general rule you should reduce risk in your portfolio, because you don’t have the time to wait out a market downturn—you need the funds to generate enough retirement income to cover your living expenses.

Risk capacity is determined by the complexity of the financial plan, and then that has to be articulated to you, the client, to make sure it’s aligned with your tolerance level.

- Have a plan for mitigating taxes in retirement

Many people are paying too much in taxes now, and may be very surprised at their tax bill once they retire, especially if they have a lot of money saved in taxable retirement accounts like traditional 401(k)s. Beginning at age 73, you are required by the IRS to begin withdrawing money from traditional qualified retirement accounts every year and pay taxes on the amounts withdrawn.

Additionally, if your “combined income” formula takes you over $25,000 in income annually, you may even pay taxes on your Social Security. The Social Security Administration estimates that 40% of Social Security recipients pay taxes on their benefits.

Of course we should all pay our fair share of taxes. But we should also create a tax plan for retirement to pay the minimum amount within federal legal guidelines, and that’s where a financial advisor in conjunction with your CPA or tax professional can help.

What you really need to watch out now for is the tax law of 2017 which will expire for the 2026 tax year. In 2026, your tax rates are going to go back up to 2017 brackets, so you need to make a plan soon.

- Make sure you have income streams that will last throughout your retirement

Planning for longevity, or living a very long time, is the fourth major pillar of retirement planning. Running out of money is a big fear among retirees, and for many people, potentially becoming a burden on family members is more of a concern than passing away.

There are strategies that are non-correlated to the stock market that can help you create a stream of income that is similar to a pension so that you have a monthly income stream in addition to Social Security that can cover your living expenses. A financial advisor trained in retirement income planning can help you look at potential income streams and what might be best for you.

If you would like to review your current retirement plan—or develop a new one—Jason Noble, CFP®, RICP® welcomes the chance to meet with you. Please call our office at 843.743.2926 or schedule a time here.

Sources:

https://www.investopedia.com/terms/i/investadvact.asp

https://www.ssa.gov/benefits/retirement/planner/taxes.html

https://finance.yahoo.com/news/trump-era-tax-cuts-set-160750197.html

This article is provided for general information only and is not to be construed as financial or tax advice. It is recommended that you work with your financial advisor, tax professional and/or attorneys when considering investments.

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd. Suite #150, Overland Park, KS 66211. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”).

030524008 JG