2022 may have been difficult, but is there reason to have a positive outlook on the future?

2022 was a challenging year for investors. Markets fell into bear market territory and experienced the worst annual performance since 2008. The S&P 500, Dow and Nasdaq declined by 19.4%, 8.8% and 33.1%, respectively. Interest rates swung wildly, with the 10-year Treasury yield jumping from 1.51% at the start of the year to a high of 4.24% before ending at 3.88%. This mirrored inflation as the Consumer Price Index climbed to a 40-year high of 9.1% in September. As a result, the Fed hiked rates seven consecutive times from 0% last March to 4.25% in December. Along the way, a myriad of other events impacted markets, from the war in Ukraine to China’s zero-Covid policy, affecting everything from oil prices to the U.S. dollar.

Despite these historical shifts in the economy and markets over the past year, the principles of long-term investing have stayed the same. Staying disciplined, diversified and focused on longer time horizons is more important than ever. For some, it may feel as if markets can’t catch a break, but this is how it felt in March of 2020 before the rapid recovery, in 2008 before a decade-long expansion, and during countless other times across history. Keeping one’s footing as markets rock back and forth is still the best way to achieve financial goals.

Below, we review five insights and headlines from the past year that can help investors to maintain a proper long-term perspective in 2023.

1. The Historic Surge in Interest Rates Impacts Both Stocks and Bonds

Beneath all the headlines and day-to-day market noise, one key factor drove markets: the surge in interest rates breaking their 40-year declining trend. Since the late 1980s, falling rates have helped boost stock and bond prices, but over the past year, the jump in inflation pushed nominal rates higher and forced the Fed to hike policy rates. This led to declines across asset classes at the same time.

While this has created challenges for diversification, there is also a reason for optimism. Most inflation measures show signs of easing, even if they are still elevated. This has allowed interest rates to settle back down in recent months even as the Fed continues to hike rates. While still highly uncertain, most economists expect inflation and rates to stabilize over the next year rather than repeat the patterns of 2022.

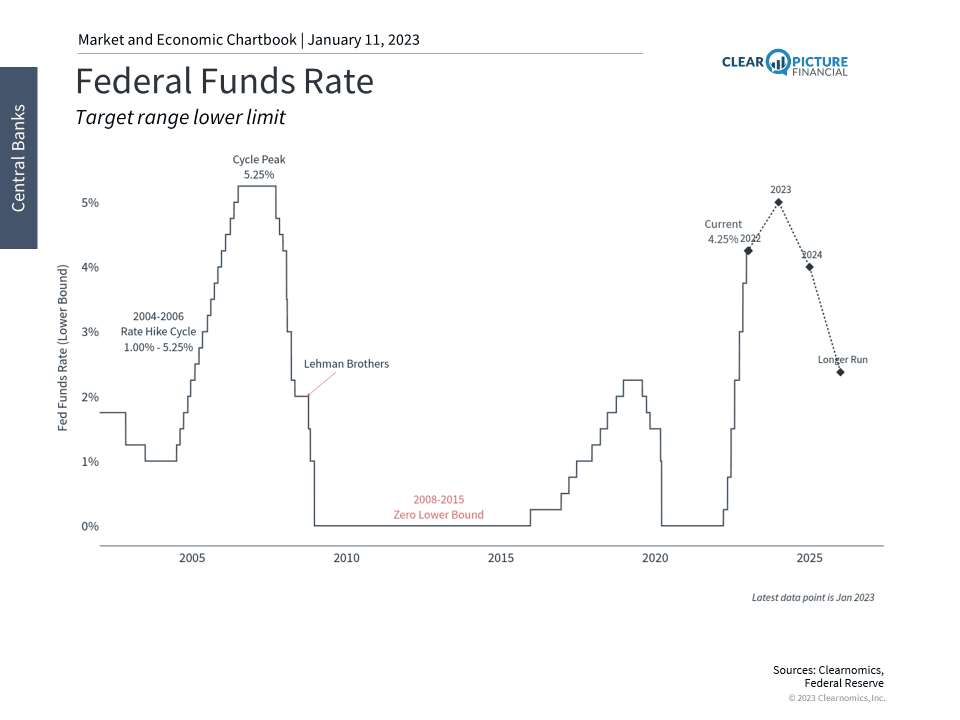

2. The Fed Raised Rates at a Historically Fast Pace

In its communication, the Fed has remained committed to raising rates and keeping them higher for longer to fight inflation. The Fed hiked rates across seven consecutive meetings in 2022, including four 75 basis point (0.75%) hikes in a row. At a range of 4.25% to 4.50%, the fed funds rate is now the highest since the housing bubble before 2008.

The central bank continues to perform a balancing act between inflation and a possible recession. Despite two negative quarters of GDP growth in the first half of 2022, few consider the economy to be in recession already. Instead, some forecasters expect the U.S. and many other countries to experience a recession in 2023. However, most also expect it to be shallow. Current market-based measures suggest that the Fed could push policy rates to 5% by mid-2023. Slowing growth may mean that the Fed takes its foot off the brake pedal sooner.

This is where the market arguably had unrealistic expectations last year. The market rally from June to August and again in October and November occurred when investors believed the Fed might begin loosening policy. When these hopes were dashed, markets promptly reversed, causing several back-and-forth swings over the year. These episodes show that good news that is supported by data can be priced in quickly but that investors should not get ahead of themselves.

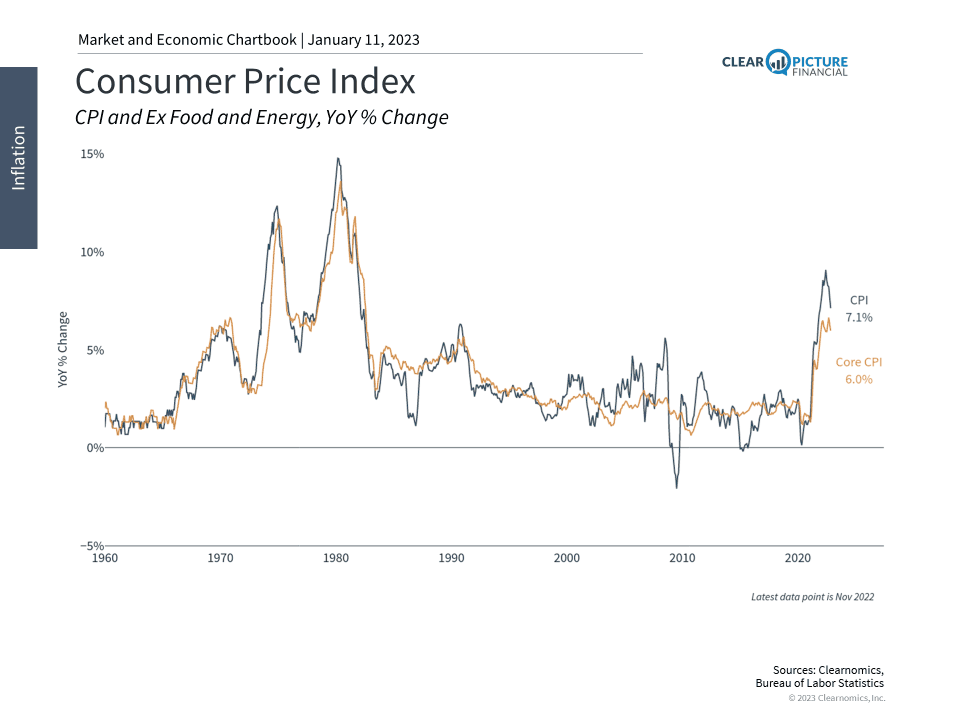

3. Inflation Reaches 40-Year Highs but Makes Small Improvements

While inflation has not been “transitory,” it may still be “episodic.” This is because the factors that drove these financial shocks were, for the most part, one-time events. Many of these are already fading as supply chains have improved, energy prices have fallen, and rents have eased. Still, the labor market remains extremely tight, and wage pressures could fuel higher prices for longer.

At this point, the direction of inflation may matter to markets more than the level. Investors have been eager to see signs of improvement across both headline and core inflation measures, and good news has been priced in rapidly. There are reasons to expect better inflation numbers throughout 2023.

4. The Rallies in Tech, Growth and Pandemic-Era Stocks Reverse

The past year also experienced a reversal of the rallies in 2020 and 2021 that were concentrated in the tech sector, growth style, and pandemic-era stocks. For the first time in years, value outperformed growth as former high-flying parts of the market crashed back to Earth as the economy slowed and interest rates jumped.

The key takeaway for investors is that diversifying across all parts of the market is important. This includes different size categories (large and small caps), styles (value and growth), geographies (U.S., developed markets and emerging markets), sectors and more. It’s also a reminder that rallies can extend for long periods, during which investors experience FOMO and pile in with little thought to risk management. Staying disciplined during these periods, which occur periodically, is essential to achieving long-term success.

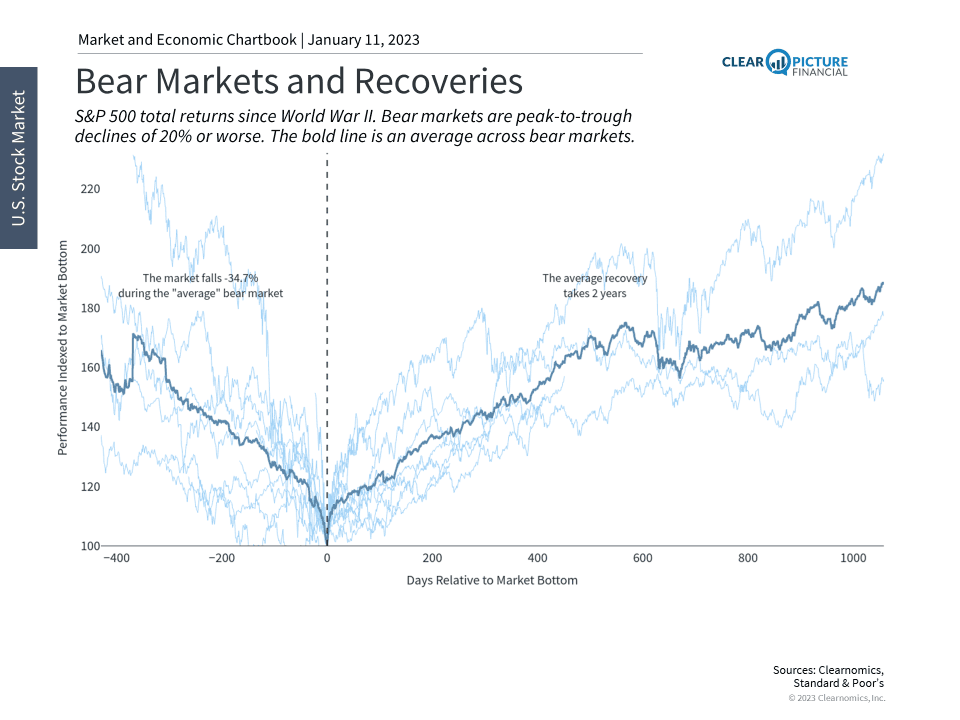

5. History Shows That Bear Markets Eventually Recover When It’s Least Expected

While 2022 was challenging, history shows that markets can turn around when investors least expect it. While it can take two years for the average bear market to recover fully, it’s difficult, if not impossible, to predict when the inflection point will occur.

Many investors wished they could go back in time and time the market. This could be true again in 2023, just as it was during previous bear market cycles. If research and history tell us anything, it’s better and easier to stay invested than to try to time the market. History also tells us it pays to be aggressive – or at least resilient – when others are fearful.

If your long-term financial plan is NOT permanently impaired by an additional 10% to 20% drawdown, then we advise staying invested at this point. If your long-term financial plan would be permanently impaired by an additional 10% to 20% drawdown, then we would advise moving into safe fixed income (short, intermediate, or even some longer duration treasuries) to maintain around a 4% current yield/income generation on the portfolio.

The bottom line? While the past year was challenging, those investors who can stay disciplined, diversified and focused on the long run will be on a better path to achieving their financial goals in 2023 and beyond. If you’d like to discuss the your financial goals, please schedule an appointment with me!