It’s no secret that the topic of retirement planning in and of itself can be overwhelming. There are so many factors to consider and despite the route you take, the final destination remains the same–as do many of the concerns.

The final destination is a lifetime of retirement income. The concerns–well, let’s break down a few common concerns folks encounter on the way with solutions to help you make it from point A to point B with your retirement intact.

Concern #1: Have I Saved Enough to Last Me Through Retirement?

Outliving their money in retirement continues to be a top concern among pre-retirees and retirees alike. Their concern may mean they ask themselves questions like:

- Do I have enough money put away?

- What do I need to have saved up in order to retire?

- Should I adjust my retirement budget or the monthly retirement income amount?

- What if something happens to me before I can make it to retirement? Would my family get the money I have saved for retirement?

- If I was late to the retirement planning party, can I catch up in any way before I retire?

- Will I ever be able to retire or will I have to work forever and if I do have to continue working into my golden years, can I do so without facing any penalties?

Concern #2: Do I Have the Right Financial Advisor?

When looking for a financial advisor or pursuing a second opinion, here are some questions you can ask yourself and your prospective advisor:

- Do I have a plan for retirement? Do I need one created?

- Do I have a budget for retirement? Do I need to amend my budget; do I have a budget right now?

- Do I have a tax plan to accompany my current financial plan? Do I have a tax plan to accompany my retirement plan?

- Do I need some help with investments?

- Do I have a legacy plan or estate plan?

- Do I have a lifetime income plan?

- How much risk am I exposed to in my plan right now? Am I comfortable with the amount of risk I am currently exposed to? How much risk do I feel comfortable with?

- Do I know how much I am paying in fees/commissions?

- Would it be beneficial to have my current plan reviewed by a fresh set of eyes?

- Should I hire a fiduciary financial advisor? What does fiduciary mean?

Because many people prioritize honesty and integrity within the advisor/client dynamic, the ‘fiduciary’ component comes into play. That’s because financial advisors operating under fiduciary responsibility are obligated, ethically and morally as well as legally to do what is in the best interest of their client first and foremost.

To narrow down the search of who might be a good fit for you or if the current advisor you’re working with might be misaligned with your future financial goals, you can begin the dialogue by jotting down a few answers to the questions above to get a better idea of where you are right now and what kind of advisor you were looking for at this juncture in your life.

Holistic and comprehensive planning for retirement is essential, and if you’re having trouble answering any of these questions, chances are you’d benefit from a conversation about your existing plan. You only retire once, so you don’t want to leave this up to chance.

Concern #3: Should I Change Course?

This is a pretty important conversation. You deserve to have clarity when preparing for retirement. You need an actual retirement plan as you get closer to retirement—a plan that has been updated to reflect your existing circumstances, financial situation, and current goals, etc. Are you in the ballpark?

Sometimes a change is not indicated. Sometimes a little self-reflection can prevent a knee-jerk decision. Are you having an emotional response to a conversation with friends or family members about saving habits, a stock tip, or economic fears? These emotional responses can crop up from time to time and tend to fizzle out, as they probably should if not based on any sound logic or reason.

However, if you are working with a broker or representative from a big box chain who has you in stocks and bonds but doesn’t really address retirement or retirement risks, you may want to make a change.

As you get closer to retirement, you may be facing too much risk given your time horizon and you may want to adjust your plan accordingly. There are also circumstances like job changes, the death of a spouse, having another child, tax vs. pre-taxed accounts, and many other issues requiring adjustment to your plans, and possibly a new financial advisor who is more focused on retirement might be a better choice for you.

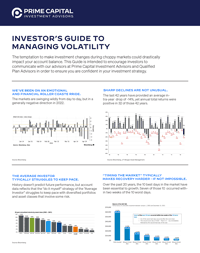

Concern #4: How Will Inflation, Recession and Other Economic Woes Impact My Retirement Preparedness?

Inflation, or the rising cost of goods and services over time, can erode the purchasing power of retirement savings. That’s why it’s important to have some of your portfolio focused on growth, while also using protection strategies to preserve your retirement income.

You can’t control inflation, market volatility or gas prices, but you can take steps to control how long your money lasts in retirement. Being proactive rather than reactive is the essence of effective retirement planning.

Making every attempt to control what you can control just makes sense. Even while we truly have little control over what occurs in the markets, you may still take steps to create and carry out effective retirement plans. You should be aware that your retirement may last for many years—even as long as two or three decades—which means that you will probably face volatile markets in the future. There are actions you can take now to help protect yourself from future downturns, like bucketing and other strategies.

Proactive Versus Reactive Examples

1) Investments aren’t keeping up with inflation

Inflation can truly erode your wealth. Diminishing purchasing power isn’t the only problem in high inflationary environments. Your investments have to work harder to hold their value in the long haul.

Reactive response: Getting so overwhelmed that you pull investments before they have been put to work for you.

Proactive response: Getting a checkup done on your portfolio with a professional in order to confirm that your investments are properly allocated and as secure as possible. The goal is a well-diversified portfolio that has just the right amount of risk for your circumstances.

2) Gifting money to your kids

Before you book that cruise for the entire family or give your child the down payment for a home, make sure you can afford to.

Reactive Response: Feeling pressure or a sense of obligation to support grown children and using your retirement account to finance their lifestyle.

Proactive Response: There is nothing wrong with gifting your children, grandchildren, or great-grandchildren money, but you do have to learn to put yourself first. Once you are certain that you have the funds you need to live comfortably in retirement, you can revisit this topic.

3) Long-term care and health care planning

The US Department of Health and Human Services estimates that upward of 70% of Americans age 65 and older will require long-term care in their lifetime.

Reactive Response: Panicking in the event of an emergency and having limited options to financially support yourself or your significant other in the event of an emergency.

Proactive Response: Adding long-term care coverage to your retirement savings plan or at least having the discussion with a professional. Now, this may mean setting aside money and building that amount on your own, adding a long-term care insurance policy, or working with a financial professional to build a tax-efficient system for your future which could be implemented through life insurance or an annuity.

4) Debt

Lingering or new debt can be a big blow to your retirement savings. It may have been easy to manage when you were collecting a paycheck, but it can hurt your cash flow and lifestyle when you’re on a fixed income.

Reactive Response: Paying all debt and prioritizing this over saving for the future.

Proactive Response: Speaking with a professional who can explain the difference between good and bad debt and how to make your plan work for you.

5) Living on pre-tax income

Taxes are a big consideration when you begin withdrawing money from your retirement savings account. If it’s a traditional 401(k) or IRA, withdrawals are taxed as ordinary income.

Reactive response: Ignoring the tax consequences until it’s too late and you learn the hard way.

Proactive response: Possibly moving and converting some of your pre-tax retirement savings into after-tax Roth IRAs, or converting a traditional 401(k) into a Roth 401(k). Roth accounts can be the right choice for some people because you don’t pay taxes on your withdrawals once you’ve had the account for five years and are 59 1/2 or older. But keep in mind that conversions are taxable events and must be planned carefully because they can’t be undone.

6) Not reviewing

Ongoing reviews can really mean the difference between retirement success or failure.

Reactive Response: Not even questioning your strategy or never revisiting it.

Proactive Response: Making sure you have a comprehensive retirement plan in place instead of just a pie chart of stocks and bonds. Your retirement plan should include the proper risk tolerance for your stage of life, a retirement budget based on your lifestyle, an emergency fund, a lifetime retirement income plan, a plan for tax mitigation, full disclosure of fees and commissions, and the proper asset allocation and diversification of your portfolio.

If you have any questions about your financial or retirement plan, please call Jason Noble at 843.743.2926.

Don’t miss Clear Picture Financial, Jason Noble’s radio show and podcast each Sunday, where you will learn how you can protect your portfolio and stay on course with your long-term financial and retirement plans. Jason and his team help retirees, those who want to retire early, and business owners who are looking for a work-optional lifestyle.

071123011 MAH/MKS

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd. Suite #150, Overland Park, KS 66211. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”).