Each week Jason Noble records his radio show, Clear Picture Financial, so that he can spread awareness and reach more people with financial and retirement information he feels is important to his listeners in Charleston, South Carolina. Here are some of the tips Jason recently shared which may help people achieve greater financial success.

- Overcome procrastination

Procrastination can interfere with productivity and success in many ways, but when it comes to your finances, procrastination can be damaging to you and your loved ones down the road. When it comes to money management, procrastination can be defined as seeing something you know you should do but are not actually doing. And while putting off things like yard work around the house may only cost you an unkempt lawn, when handling your finances there is often a real dollar cost to putting off financial planning.

Can you overcome your own procrastination when it comes to finances? Yes. Will it involve a commitment and effort on your end? Yes. Is it hopeless or “too late” to start? Not by a long shot.

Even if you feel like you’ve hit the point of no return due to a lack of proper planning, don’t be tempted to throw in the proverbial towel. When it comes to your finances, you can make the decision to start now. Just take baby steps toward making things right.

The first step to overcoming procrastination is to take an honest and realistic assessment of where you are right now versus where you want to be. Taking a comprehensive look at your financial situation is essential to creating the forward momentum that will get you down the road toward your future. Don’t be afraid to take stock of your situation.

And remember, when you decide to take those initial baby steps and get out of the procrastination mode, don’t overdo it. Give yourself time to get adjusted to figuring things out. Don’t shy away from getting a handle on your financial future simply because you feel like things are too far gone. Address it one step at a time.

- Avoid late payments and fees – and manage your debt

Late payments come with high fees, and multiple late payments not only take money right out of your pocket but also put you at risk of a damaged credit rating, which can take years to repair. Instead of falling victim to this cycle, you can take proactive steps toward paying down your debt. Start with an honest assessment of your debt, create a strict budget for yourself and limit spending which you can put toward reducing your debt.

Remember, if you are in credit card debt, you are not alone. Data from the Federal Reserve for the second quarter of 2023 revealed that credit card debt soared to $1.03 trillion with interest rates hovering between 20-27%. So, yes, it can certainly be challenging to handle the debt you’re faced with. On average, Americans carry around $5,733 in credit card debt according to TransUnion’s latest data.

It never hurts to ask for a lower interest rate when dealing with your credit card companies. In fact, according to a recent LendingTree report, 76% of people who asked for a lower interest rate on their credit card were granted that request. Sitting down and creating a system for tackling debt and restructuring your financial hierarchy of needs could be incredibly beneficial to your overall financial well-being. A financial advisor who is a financial planner can be very helpful in this regard.

Write everything down. How much debt do you have to get under control? What interest rates are you paying to each debt holder? Should you pay off one card first or make multiple payments as the best course of action? It’s important to establish a sturdy financial foundation by chipping away at your debt systematically.

- Plan for a long retirement

Many Americans spend their lives working hard and dreaming of the day they can finally retire. But planning for retirement requires more than dreaming. It’s all about the plan.

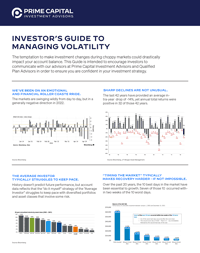

Back in the 1930s, when the Social Security pension system was first implemented, life expectancy at birth was 58 for men and 62 for women. With the retirement age of 65, the majority of people didn’t live very long in retirement—if they even made it at all.

Today’s retirement looks much different than it used to. A 65-year-old male can expect to live another 17 years on average; a 65-year-old female another 19.8 years. Retirement planning is essential to help ensure adequate funds are in place to cover future housing, food and health care costs, including inflation.

According to a TD Ameritrade study, 81% of Americans are shifting assets in preparation for living longer than their ancestors did by reducing expenses, buying secured life insurance and maximizing their contributions to retirement plans. Financial advisors and planners who focus on retirement are familiar with what’s required to make retirement funds last with today’s longevity, and they can help people create distribution and retirement income plans which can kick in after retirees have stopped working and receiving paychecks.

- Avoid withdrawing or borrowing retirement funds prematurely

People may fail to understand the consequences for tapping retirement accounts and may access those funds without a second thought. A recent TD Ameritrade survey showed that 44% of Americans ages 40 to 79 have taken money out of a retirement plan!

Unfortunately, “borrowing” from your retirement savings is not only detrimental to you later on, but there are significant tax penalties associated with making early withdrawals that can affect you now if you are younger than 59-1/2, and taxes are owed on the withdrawn money in the year it’s withdrawn if it’s taken from a taxable account like a traditional 401(k) or IRA.

Remember, you are denying your future self the benefits of compound gains / interest by drawing from retirement accounts early—in addition to potentially paying penalties plus additional income taxes to the IRS. So, there are no real benefits to these withdrawals.

Instead, create an actual emergency fund in a separate, liquid account (i.e. a bank savings/checking account that’s free from early withdrawal fees or penalties) for emergencies rather than dipping into retirement funds. Keeping this money in a separate account helps ensure money is there for rainy days and won’t be easily accessed for other non-emergency expenses.

- Create contingency plans for risks

Speaking of emergencies, what would you do if your back was against the wall? If you lost a job, lost an income, lost physical or mental capacity, or lost a spouse or child? Risk management helps you identify risks which can blow up a financial plan and put you and your family in danger of losing everything. Shifting risks away from you and over to insurance companies or other methods of coverage or backup planning can make all the difference.

Oftentimes, folks may not plan for their future because they don’t want to face or address the potential risks, or even look at their finances in the present. It’s no secret that inflation, interest rates and living expenses are challenging folks across the country. Unfortunately, this is precisely why you need to have a plan in place should you find yourself in a precarious situation as it relates to your finances. What is your backup plan if things go south? What account would you draw from first? Not having a plan can expose you to more financial hardship down the road.

Remember, you could be forced into retirement before you’re ready. While it’s nice to have a plan for retirement, sometimes life has other plans. Fifty percent of people surveyed by TD Ameritrade said that they had to retire before they truly wanted or planned to, due to layoffs, responsibilities as caretakers and unexpected changes in their financial situation and health issues.

Additionally, you need a plan for long-term care if you need it, as 70% of Americans do in some form in their lifetime according to the U.S. Department of Health and Human Services. If that involves an assisted living facility, the costs can be incredibly high, and Medicare will not cover them.

- Stop mindless spending—create a realistic budget

If you don’t know how much you are spending versus saving, that can be detrimental to your financial future. When you look at how much you are allocating to your savings, your emergency fund, your bills and monthly expenses, you can always make adjustments that will help you down the road.

This becomes possible when you create a budget. To start your budget and begin diverting some unnecessary spending to saving, take a comprehensive inventory of your subscriptions, whether it be streaming services, apps for your smartphone and other weekly/monthly/annual outgoing payments from your accounts. This affords you the opportunity to regain control of your finances, unsubscribing from services that you no longer need or use and the ability to siphon off some of those dollars for your future. You can then repurpose those funds, whether it’s by stashing those dollars into investment vehicles or into your emergency fund. This step is a pretty feasible way to reframe the way at which you spend money and manage money going forward.

- Meet with an advisor

Sit down with a financial advisor and professional retirement planning coach and see what kind of plan they would apply to your personal circumstances. You’d be surprised at how many people just need a little support and guidance to get the ball rolling. A financial advisor is a professional who is trained and involved with the financial industry every single day, and they work with dozens of different clients facing various financial issues and challenges and retirement scenarios. Trying to wing it by yourself with no experience, no training and no support may not make sense, and may not get you the results you want.

Jason Noble is a fiduciary financial advisor who focuses on retirement. He has been named fifth in the nation as one of the top 100 solo advisors to watch in 2023 by AdvisorHub. If you would like to discuss your financial and retirement plan, you can set up a consultation with Jason by calling our office at (843) 743-2926.

Sources:

- https://www.reuters.com/world/us/us-household-debt-largely-unchanged-q2-credit-card-balances-jump-ny-fed-says-2023-08-08/

- https://www.cnbc.com/2023/06/09/how-much-credit-card-debt-americans-hold-by-age.html

- https://www.lendingtree.com/credit-cards/study/lower-apr-requests/

- https://www.ssa.gov/history/lifeexpect.html

- https://www.statista.com/statistics/266657/us-life-expectancy-for-men-aat-the-age-of-65-years-since-1960/

- https://finance.yahoo.com/news/jaw-dropping-stats-state-retirement-200025720.html

- https://sports.yahoo.com/jaw-dropping-stats-state-retirement-160010873.html

- https://acl.gov/ltc/basic-needs/how-much-care-will-you-need

This article is provided for general information only and is not to be construed as financial or tax advice. It is recommended that you work with your financial advisor, tax professional and/or attorneys when tax planning.

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd. Suite #150, Overland Park, KS 66211. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”).

091323002 MAH