Pensions will be recalculating within the next couple of months

One of the biggest decisions one must make close to retirement is whether to take your pension benefits as a lump sum or as an annuity over time. There are many variations to determine which is best, and not one answer is good for everyone, as this is a very personalized decision. Some but not all factors that are needed to be taken into consideration are your health, family’s health history, the financial stability of the company and their pension’s strength. Also, if you are married, what is the age gap, what is your spouses’ health and their family’s health history. Finally, another important item worthy of considering is, what are the interest rates. So why does this matter and how does this impact me? Let’s dive in deeper, and know it’s best to speak with a qualified professional to determine the best course of action for you!

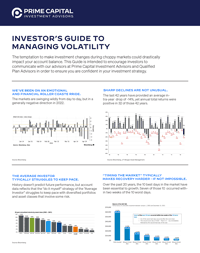

If you are leaning towards the lump sum payment over the annuity, please note the higher the rate used to calculate a lump sum the smaller your payout. This is done due to how it is calculated actuarially to make it equivalent to the annuity. The specific IRS-published interest rates, based on the corporate bond yield curve, is what is used in the company’s lump sum calculation. This is what has been rising, thus lowering the lump sum payouts.

Let’s use this illustration to show what I mean: If the rate used is 3%, a pension benefit of $6,000 monthly ($72,000) over 25 years would yield a lump sum of roughly $1,253,746. All things being the same, except now the rate used is 6%, the lump sum payout would be about $920,401, a difference of $333,344! That is a 26.5% reduction in benefits, all due to higher interest rates!

It is important to note that the annuities are not directly impacted by higher interest rates, as those payments are generally determined by a calculation, based on your age, years of service and salary. Their pre-determined formulas provide a fixed amount per year. The issue with the annuity is that the amount is fixed, and does not account for inflation eating away the purchasing power of the annuity payouts. Many company plans don’t include an annual cost-of-living adjustment (although state and local government pensions may have this included). Another issue with the annuity decision is if you pass away prematurely, depending on how you structured the annuity, there is no money left to your spouse and or beneficiaries.

A quick example of how this works: A 1% annual rate of inflation would reduce the value of a $30,000 pension to $23,335 in 25 years. A 2% annual rate of inflation would lower the purchasing power to $18,104.

As you can see, this is a very important topic for those that are eligible for a pension, which is estimated to be 15% of Americans.