Jason Noble was recently featured on Forbes in an article titled, “How Can 401(k) Plan Sponsors Address The Biggest Issues They Face Right Now?”

When it comes to 401(k) plans, even small or modestly-sized businesses can benefit—if they have all the right pieces in place.

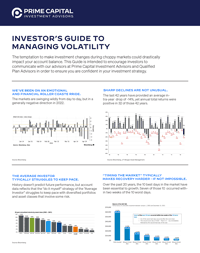

A 401(k) plan can allow a business owner to not only save for their own retirement, but to attract and retain top talent by having a desirable employee benefit in place. And there are tax benefits and breaks available to businesses who have 401(k) plans.

According to the Department of Labor (DOL), there are four initial steps for setting up a 401(k) plan:

- Adopt a written plan document,

- Arrange a trust for the plan’s assets,

- Develop a recordkeeping system, and

- Provide plan information to employees eligible to participate.

Plan sponsor (employer) fiduciary responsibilities

Setting up a 401(k) plan correctly is one thing, but becoming a 401(k) plan sponsor also incurs a fiduciary duty to the plan’s participants.

The Employee Retirement Income Security Act of 1974—referred to as ERISA—requires that a specific plan administrator be named for a 401(k) plan. For smaller businesses, this is usually the owner or a high-level executive.

Fiduciary responsibility means taking on important financial and legal duties. From the Forbes article, there are still a lot of 401(k) plan sponsors who don’t really have a good working knowledge of their responsibilities as fiduciaries or the skillsets internally to prudently evaluate issues, set goals and make decisions for their 401(k) plan.

Hiring the right people

As an entrepreneur, you may be used to doing a lot of things yourself. But running your 401(k) plan really shouldn’t be one of them. Being a plan sponsor takes a lot of time, from “ongoing administrative tasks, to 5500 and audit prep, to regular retirement committee meetings, to new IT security audits.”

Between other people in your company and/or outside vendors, you can get help to cover many of the tasks you’re responsible for. For instance, you can set up a plan committee or committees with charters defining their meeting schedules, responsibilities and legal reporting obligations.

Additionally, you should consider having a responsive Third Party Administrator (TPA) who will address issues and questions unique to your plan and your role as plan sponsor.

Encouraging participation

Small employers often don’t have the resources for an on-staff human resources team with an understanding of the complexities of the 401(k) ecosystem, yet employee participation is the crux of a healthy 401(k) plan. Having a seasoned advisory firm onboard to address ongoing employee participation issues can really help.

Jason Noble says:

“A big issue 401(k) plan sponsors face with their own company is that the plan sponsors get feedback from the employees on things or services they would like to see within the plan, but the company does not want to invest in making those changes. Those changes can cost money and time, so having a regularly scheduled meeting to discuss the feedback from the employees between the plan sponsor and their own company’s leadership team would be an important way to address these items on an ongoing basis. Human Resources knows the voice of the employees can get loud, but does that voice get to leadership? These meetings will help with this issue!”

If you’d like help with your 401(k) plan, Jason Noble and his team at Prime Capital Investment Advisors have years of experience managing small, medium and large 401(k) plans. We can help you set up a plan, or review your current plan to see if we would recommend any changes. Call Jason at (843) 743-2926.

Read the entire Forbes article here.

92722009 MKS

Advisory products and services offered by Investment Adviser Representatives through Prime Capital Investment Advisors, LLC (“PCIA”), a federally registered investment adviser. PCIA: 6201 College Blvd. Suite #150, Overland Park, KS 66211. PCIA doing business as Prime Capital Wealth Management (“PCWM”) and Qualified Plan Advisors (“QPA”).